Thank you Brexit for the moves you generated in the S&P, bonds gold and currencies but I am a little disappointed that’s all you had in you.

The UK economy is 3.94% of global GDP, we got more play out of Greece, an economy equivalent in size to Orange County California.

Pound shorts were decent, less than expected, the Swiss moved more when they defected.

FTSE 100 shorts were a bore

Dax shorts you could ignore S&P 500 shorts couldn’t gather momentum I’ve seen better moves generated by Fed intentions.

S&P 500 shorts couldn’t gather momentum I’ve seen better moves generated by Fed intentions.

A $3.00 drop additional pumping has out do this $3.00 pop and were sitting at $48 like nothing happened.

Gold that loves bad news didn’t even make the news

Even though the moves generated by Brexit were disappointing, there is an upside Brexit was yet another crack in the dam of poorly constructed global policy decisions.

I believe this policy dam will break generating major market moves that will rival anything we’ll see in our trading careers.

We all can see the US debt typhoon clearly on the horizon. We all know if rates normalize as Yellen represents the US can’t afford to refinance its maturing debt much less new issues that need to be sold finance new debt.

After this last blast to the upside I can’t see anyone buying low yield US debt? The dollar is near a 10 year high, instruments prices are at all time highs, currency and instrument risk in one hour is more than than annual yields?

Banqiao Central Bank policies

Over the last several decades Central Bank Monetary policies in majority have been hastily created by appointed academics anxiously awaiting the opportunity to test their hypothetical economic theories based more on ego & arrogance than “real world” work experience.

Their inexperience and arrogance led this fester of academics to believe they could actually solve the debt crisis by making the debt crisis even larger.

The harsh reality is the US has the worst debt to tax receipt ratios in history, the worst credit rating in history and the most miscreant reporting by governmental agencies on economic statistics such as inflation and labor in history.

Envision Central Bank/Fed policy to a Dam holding back the debt crisis and name it after its hydrology counterpart the Banqiao.

The Banqiao Dam was hastily designed by academics using unproven hydrology theory with ½ as many gates as recommended. Academic theory enabled the dam to be built in a shorter period of time to solve the long term problem of unmanageable flooding in the Huai river basin which peaked in 1949 & 1950.

Construction of the Banqiao dam began in April 1951 and was completed in June 1952. Aside from a few figureheads the Banqiao dam was designed by academics with impeccable credentials but lacked the actual work experience in hydrology.

In the in the 1950’s & 1960’s the Government acknowledged the Dam might some “minor” structural issues as it was in majority made out of clay. They also acknowledged it cost multiple times what was represented and dam wasn’t expected to work as originally represented. In the coming decades more money was spent on trying to repair the dam than the cost of a new one.

The ambiguous tone, unfounded optimism in the Banqiao dam reports is very similar to what is currently being used by Central Bankers to explain why their economic recovery programs haven’t worked as expected despite costing multiple times what was represented.

The US debt to tax receipt ratio is a perfect example of the Fed’s economic recovery “design flaw”.

Red = Federal debt

Green = Debt service on the national debt

Blue = Debt held by Federal Reserve Banks

Black = Federal government receipts from personal taxes

Grey = Federal government receipts from corporate taxes

Source Federal Reserve

In the 1950’s through 1970’s The Chinese government told residents not to worry as a team of skilled professionals with the help of the Soviets was deployed to monitor and resolve any issues with the dam, they told residents to feel safe despite the weight of water behind the dam and patient.

From 2008-2016 the US Government has told its residents not to worry as a team of skilled professionals (the Fed) has been deployed to resolve any issues with the Economy, to feel safe about the weight of debt behind the “economic stimulus” dam and to be patient during “economic recovery”.

Actual pictures of the Fed team with their linked bios on this Seeking Alpha page

Typhoon Nina landed onto the scene with a bang in 1975, hitting China hard and quickly destroying the Banqiao Dam.

The dam collapsed killing approximately 26,000 people from the initial flooding and another 145,000 during subsequent epidemics and famine. 5,960,000 buildings collapsed, 11 million residents were affected. Unofficial estimates of the number of people killed by the disaster have run as high as 230,000. The collapse of the Banqiao Dam led to such great flooding that it set off a series of dam collapses throughout China, greatly magnifying the damage.

Over the last 24 months the Federal Reserve has lowered its expectation for where they see the Fed Funds rate they set by December 2018 from 3.75% down to 2.50%. With each reduction in rate expectation they are confirming the failure of their policies

During the latest Fed “guidance” Yellen again confirmed that the Fed’s projections for the economy and interest rates were wrong. Yellen predictably regurgitated the same pathetic rhetoric feed to her by her keepers about “low” inflation, meaningless timelines for interest rate hikes and then tells us to be patient while failed Fed polices continue to destroy the US’s economic future.

June 2016 “ rates will be 2.50% by December 2018, “economic recovery” is taking longer than expected, inflation is lower than expected.

March 2016 ” rates will be 3.00% by December 2018, economic recovery” is taking longer than expected, inflation is lower than expected.

December 2015 ” rates will be 3.25% by December 2018 “economic recovery” is taking longer than expected, inflation is lower than expected.

September 2015 ” rates will be 3.50% by December 2018, “economic recovery” is taking longer than expected, inflation is lower than expected.

September 2014 ” rates will be 3.75% by December 2018, “economic recovery” is taking longer than expected, inflation is lower than expected. (Yes she’s wearing the same outfit)

Source Federal Reserve

The math on “economic recovery”

The US debt to GDP ratio is currently the worst since World War II at 105% and is quickly closing in on the all time high of 113%

- Current debt to GDP ratio 105%

- Debt to GDP in 2009 when “economic recovery” officially began 80.10%

- Debt to GDP at the height of the Great Depression 39%

- All time high debt to GDP during World War II 113%

Source Federal Reserve

Source Federal Reserve

Budget deficits still exceed 400+ billion annually. Each 1.00% increase in debt service could add 192 billion to the current 400+ billion annual deficits.

Source Federal Reserve

Source Federal Reserve

The Tax receipt growth to Federal debt ratio is by far the worst in history.

From 2008-2015 the US national debt increased by 104% while tax receipts increased by only 36%.

Red = National debt

Black = Personal income tax receipts

Blue = Corporate tax receipts

Source Federal Reserve

Source Federal Reserve

The worst debt to personal income ratio in history

Red = National debt

Green = Personal income

Source Federal Reserve

Source Federal Reserve

The worst debt to employed population ratio in history.

Red = National debt

Green = Non Farm Payroll

Black = Total Population

Source Federal Reserve

Source Federal Reserve

Millions in the US annually are still losing their homes.

- US Mortgage delinquency rates remain at 6.16% in 2016

- 6.16% is nearly twice the pre recession all time high of 3.36%

- Nearly 3 times the pre recession average of 2.24%

Source Federal Reserve

Source Federal Reserve

Home ownership in the 21st century is at a new all time low.

Source Federal Reserve

The worst trade deficits on record, over 5 trillion has left the US for foreign shores since “economic stimulus and recovery” began.

- From 1960 to 2007 the cumulative trade deficit was 7.73 trillion US dollars

- From 2008 to 2016 5.13 trillion

- Cumulative total increase from 2008 to 2016 66.31%

Since 1960 12.86 trillion in wealth has transferred from domestic to foreign accounts.

Source 1960-2013 Federal Reserve

Source 1960-2013 Federal Reserve

Source 2014-2016 Trading Economics

“Quantitative Easing”

“Quantitative Easing” created 4.19 trillion dollars with keypunch entries backed by no tangible assets or income flow to;

- Bail out the banks that facilitated the debt crisis

- Purchase record amounts of US Federal debt that no one else would buy at non competitive interest rates

- Force and hold rates at historic lows enabling the US Treasury to finance over 10 trillion in new Federal debt at the lowest rates in history.

4.19 trillion is nearly 5 times greater than total Federal debt was during the “inflationary debt crisis” of 1980 when short term rates soared above 18%.

1980 Federal debt = 863 billion ( 2.50 trillion in 2016 dollars)

2016 Federal debt = 19.23 trillion

Fed’ balance sheet

Red = 2.46 trillion in US Treasury

Green= 1.73 trillion in bad bank debt

Source Federal Reserve

Source Federal Reserve

The US now has the worst debt rating in its history

13 countries now have a higher debt ratings than the US, most have the same or higher deposit rates.

China by the Fed’s own numbers buried the US during “economic stimulus & recovery”

The worst growth ratio on record against China

Blue = US GDP Growth

Red = China GDP Growth

Source Federal Reserve

Source Federal Reserve

The worst debt to GDP ratio on record .

Blue = US Debt to GDP

Red = China’s Debt to GDP

Source Federal Reserve

Source Federal Reserve

The “balance” of trade was beyond ugly

Blue = US “Balance” of Trade

Red = China’s “Balance” of Trade

Source Federal Reserve

Source Federal Reserve

The widest spread on record between the US’s and China’s short term interest rates

Source Federal Reserve

Source Federal Reserve

During “economic stimulus and recovery” the USD had an overall depreciation of 10.27% against the Chinese Renminbi despite massive intervention by the Chinese to devalue their currency.

Source Federal Reserve

Source Federal Reserve

The World Bank tells us China’s economy will surpass the US’s by 2019

Source World Bank

What “economic stimulus” did for savers

Over the last 8 years artificially low rates have stripped savers and the free market economy of trillions of dollars in interest income through the largest negative rates of return in history.

How does stripping savers and the free market economy of trillions of dollars to save the US Treasury the same amount in debt service cost stimulate an economy and foster economic recovery? It doesn’t and never will.

Red = The BLS.GOV reported Consumer Price Index (CPI)

Black = 3 Month deposit rates

Blue = 3 month deposit rates outside the Treasury system

Green = 2 year deposit rates

Source Federal Reserve

What “economic stimulus” did for banks

While savers were being stripped of trillions the same banks that facilitated the debt crisis received trillions in Fed bailouts.

It gets worse

Since 2009 the Fed has permitted banks to gorge on the largest gross profit margins between bank borrowing cost and lending rates in history transferring these trillions from consumer balance sheets directly to bank balance sheets.

In 2009 when the Fed Funds bank borrowing rate dropped to 0.13%, the prime rate remained unchanged at 3.25%, then rose to 3.50% December 2015.

Consumer credit card rates during “economic stimulus and recovery” never had a meaningful decline remaining above 13.00% since 2009, very close to the 20 year average of 14.22%.

How does overcharging consumers trillions in inflated borrowing costs to benefit the same banks that caused the debt crisis stimulate an economy and foster economic recovery? It doesn’t and never will.

Fed Funds bank borrowing rate relative to bank lending rates

Red = Fed Funds bank borrowing rate

Black = Prime lending rate

Green = Average credit card rate

Blue = 30 year conventional mortgage rate

Source Federal Reserve

Source Federal Reserve

Not that Japan is any example to follow but when Japan’s deposit rates went to zero the Japanese had the conscience to lower their prime lending rate to 0.95%

At 0.95% Japan’s Prime Rate is less than 1/3 of the 3.00% gross profit margin spread between the US Fed Funds bank borrowing rate and the US Prime rate.

Source for the Bank of Japan

What economic stimulus did for the US Treasury

- Enabled the Treasury to finance over 10 trillion in new deficit spending at the lowest rates in history.

- Allowed the US Treasury to refinance existing Federal debt at the lowest rates in history (Maturity Extension Program)

- Lock in the US Treasury’s debt service cost at the lowest rates for the longest period of time in history the average, Treasury duration is now nearly 6 years, average yield less than 2.75%

Red = Federal Debt

Blue = Federal Debt Held by Federal Reserve Banks

Light Blue = Social Security

Green = Federal debt service cost that the Fed has stopped reporting

Source Federal Reserve

Source Federal Reserve

Fed fiction is nothing new

For over a 1/2 a century the Federal Reserve, US Treasury and Bureau of Labor and Statistics have relentlessly worked together to “stabilize and preserve” the US financial system.

In the 1960’s Fed Chair William McChesney Martin was facing inflation and escalating Federal deficits, Martin using the independence gained with the Treasury-Fed Accord begin creating the “new” Federal Reserve.

1970 Arthur Burns became Fed chair, by 1971 he along with president Nixon took the US dollar off the gold standard and the dollar became a “fiat” currency. (Fiat currency = a currency backed by no tangible asset or income flow)

1971 Publicly Burns made himself out to be an inflation hawk. He testified that the Fed was “determined to follow a course of monetary policy that would permit only moderate growth in money and credit,” making it “possible for the fires of inflation to burn themselves out.”

Didn’t happen, during his eight-year tenure as Fed chair Burns failed to control prices by 1974 inflation was above 12% and the average during eight-year was an unprecedented rate of 6.5%.

Orange = BLS.GOV Consumer Price Index

Purple = Total Imputed Interest Paid

Red = Federal Debt

Blue = M1 Money Supply

Source Federal Reserve

in 1974 several Fed members approached the BLS.GOV and began persuading them to begin penciling out ways of revising the BLS.GOV releases to more “accurately” report inflation and employment.

Higher rates and minor BLS.GOV revisions pressured the inflation rate from 12% to below 6% by 1976. Investors started believing that maybe a currency backed by no tangible asset or income flow could actually work for the largest economy in the World.

Source Federal Reserve

Between 1971 and 1980 the US Federal debt grew from 424 billion (2.504 trillion in 2016 dollars) to 863 billion (2.505 trillion in 2016 dollars)

Source Dollar valuations, Bureau of Labor and Statistics.

Source Federal Reserve

January 1977 precious metals investors choose to ignore the Keynesian economic models advocated by many Fed voting members.

Keynesian economic models (prior to their current revisions) did not take into account the inflationary implications of the horrific budget deficits that were being generated by the US since it abandoned the gold standard in 1971.

The price of gold rallied

$132.10 January 1977 ($521.56 in 2016 dollars)

$197.50 to a new all time high by July 1978 +49.51%. ($724.76 in 2016 dollars)

By January 1980 gold was trading at $843.00 up 538.15% ($2,447.78 in 2016 dollars)

Source Dollar valuations, Bureau of Labor and Statistics.

Source Federal Reserve

Inflation, Treasury rates and debt service costs all soared

Source Federal Reserve

1979 with the US dollar now a “fiat” currency it looked doomed, nearly every tangible asset on the board rallied against the US dollar, speculation frenzied, 100’s of millions were being made and lost in minutes.

As gold and silver moved sharply higher in 1979 bullion banks were facing “fails to deliver” on their open contracts. Bankers, the Fed, US Treasury and exchanges were panicking.

August 1979 Paul Volker is appointed chair of the Federal Reserve

Volker began a series of very aggressive rate hikes to contain inflation as it approached 14.80%. (April 1980)

Source Federal Reserve

1980 rule change

Two brothers from Texas who nearly cornered the silver market and tax straddle billions in profits into the following tax year provided the Federal Reserve, US Government, Bankers and Exchanges the excuse they needed to enlist the CTFC and IRS to change the rules for trading and taxation on trading US markets.

Position limits

Liquidation only

1256 Tax rule

At the same time the BLS.GOV was given the “all clear” to use “revisions” more aggressively ” to more “accurately report” inflation and employment.

By 1983 Volker was hailed as a hero because the cumulative impact of his tight monetary polices and BLS.GOV inflation calculation revision magic had dropped the reported BLS.GOV inflation from it’s peak of 14.80% in 1980 to under 3% by 1983.

This video tells the story in 2 1/2 minutes

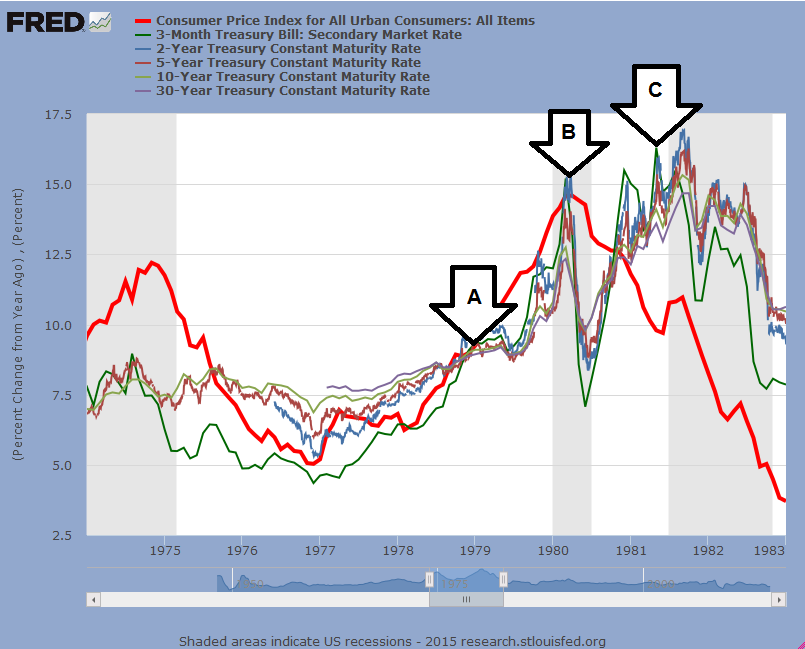

The interest rate market’s reaction to the cumulative policy decisions and rule changes .

A) 1979 Volker begins a series of aggressive rate hike, the curve inverts with short term rates exceeding long term rates

B) 1980 trading and taxation rules change and “Revised” BLS.GOV inflation calculation magic engages.

C) After a decade of high inflation it magically lowers from 14.80% to less than 3.00% containing Federal debt service cost and all increases in governmental expenditures that are linked to the “official” CPI such as Social Security.

Source Federal Reserve

Coincidentally in every period since the late 1970’s when the US has had an inflation, debt or employment crisis we’ve seen revisions as to how the BLS.GOV does their calculations. The more significant the problem, the more significant the revisions.

1987 Alan Greenspan is appointed Chair of the Federal Reserve,

1990 the BLS.GOV implements another round of major revisions to the CPI.

With inflation “contained”Greenspan endorsed easy-money policies at the Fed which fueled the subprime mortgage market.

Greenspan Left the Fed 31 January 2006 and Bernanke was appointed the new chair.

Greenspan’s agenda one week after leaving the Fed.

7 February 2006 Lehman Brothers paid Greenspan $250,000 to meet with 15 of its most important hedge fund clients in Lehman’s executive dining room. Greenspan’s primary theme was the white-hot U.S. housing market was slowing down but evidence of it would not show up statistically for several months and it could take more than a year.

Housing prices fell, global investor demand for mortgage-related securities evaporated, many of the attendees at the 7 February 2016 Lehman’s Brothers dinner that negated Greenspan’s advice watched their hedge funds implode as subprime mortgage failures ignited the largest financial crisis in US history.

15 September 2008 Lehman Brothers filed for bankruptcy, at the time it was the largest BK in history, as its assets far surpassed those of previous bankrupt giants such as WorldCom and Enron.

In the video below Greenspan apologized for nearly 2 decades of failed monetary policy that put the US into the largest financial crisis in history but kept Lehman’s 250K fee and still earns over 100K per “speaking engagement”

From bad to worse

31, January 2006 Bernanke becomes Fed chair, his bio and his clueless calls on the market that earned him the job to navigate the US out of crisis.

By March 2006 Bernanke had led the Board of Governors of the Federal Reserve System to cease the publication of the M3 monetary aggregate. The Board also ceased publishing the following components: large-denomination time deposits, repurchase agreements (RPs), and Eurodollars.

2007 the debt crisis fully engages, the oldest and largest Wall Street firms are facing insolvency.

2008 Bernanke fires up the Quantitative easing printing press creating 600 billion with keypunch entries to buy bad bank debt and cauterize the sub-prime mortgage hemorrhages for the “to big to fail” institutions.

With the creation of 100″s of billions inflation began rising but BLS.GOV CPI revision magic contains it.

By 2009 the US Government completely disengaged from trying to make the tough policy decisions that would be in the best long term interest of the United States and opted to use the “Quantitative Easing” printing press and BLS.GOV revision magic to give the World the impression the US economy was on the right track.

June 2009 the “Great Recession” officially ends and “economic recovery” begins

True inflation versus BLS.GOV fiction

The CPI was originally created in 1919 to help businesses, individuals and the government adjust their financial planning for the impact of inflation. The first round of major “revisions” to the CPI occurred in the late 70’s and early 80’s after the Federal Reserve and US government had exhausted all ethical options to contain US inflation since the US abandoned the gold standard in 1971.

In the decades that followed the BLS.GOV reporting system has increasingly succumbed to pressures from miscreant officials who have the intent of reducing US government debt service cost and all governmental expense increases that are tied to the official CPI rate (Military, Social Security, Government Employees and Welfare recipients)

The CPI now consists of more than 80,000 items in over 200 categories arranged into eight major groups, “Hedonic Quality Adjustments” are applied then the data is “weighted” to reflect a “more accurate” representation of inflation.

As this index was in part created to help government “adjust their financial planning for the impact of inflation” let’s match the BLS.GOV CPI inflation calculations between 1978-2015 to actual totals for Federal, State, and Local Government spending

In 1978 total spending was $734,467.0 million

| 1 | Total Spending | $734,467.0 million |

| 2 | Pensions | $114,391.6 million |

| 3 | Health Care | $66,243.2 million |

| 4 | Education | $127,181.0 million |

| 5 | Defense | $130,939.0 million |

| 6 | Welfare | $70,465.9 million |

With the BLS.GOV’s budget at 618.2 million annually one would expect the BLS.GOV to produce fairly accurate numbers.

BLS.GOV calculations show that total spending between 1978 to 2015 should have increased by 1,935,489 million or +263.52%.

The actual increase was 5,627,678 million or +766.23%

| 2015 | 1978 | Increase | Percent | ||

| 1 | Total Spending | $6,362,145.20 | $734,467.00 | $5,627,678.20 | 766.23% |

| 2 | Pensions | $1,240,552.20 | $114,391.60 | $1,126,160.60 | 984.48% |

| 3 | Health Care | $1,357,831.00 | $66,243.20 | $1,291,587.80 | 1,949.77% |

| 4 | Education | $1,015,198.70 | $127,181.00 | $888,017.70 | 698.23% |

| 5 | Defense | $798,736.90 | $130,939.00 | $667,797.90 | 510.01% |

| 6 | Welfare | $466,372.50 | $70,465.90 | $395,906.60 | 561.84% |

Source USgovernmentspending.com

Now let’s match the actual increases to gold

Average price of gold from January 1976 to December 1978 = $155.28

Average price of gold from January 2013 to December 2015 = $1,278.46

Increase = $1,123.18

Percent increase = 723.32%

Summary

BLS.GOV calculations say the increase should have been +263.52%.

Actual increase +766.23%

Gold standard increase +723.32%

Source Federal Reserve

You can take nearly any period on anything from home prices, oil, food, college tuition stocks or funeral costs and the BLS.GOV calculations on this page will underestimate the actual increase by a significant amount.

The big difference

Current calculations try to measure the minimum cost of living.

Pre-1980 calculations measure a constant standard of living.

Blue = Pre 1980 CPI calculation methods (constant standard of living)

Red = Current current CPI calculation methods (minimum cost of living)

Source Shadow Stats

My experience with US inflation

I run a family office from a tax free spec of an island 1,770 kilometers south east of Palm Beach Florida. As the head of a family office my job is the preservation and enhancement of family wealth I keep a close eye on expenditures to ensure a constant standard of living rather than a minimum standard of living.

Over the past 20+ years my family and I spend several months per year in the US, my family has purchased the same items, same amounts of food, alcohol, drugs, energy, resided in the same zip code and had the same household staff.

BLS.GOV inflation calculations put my increase over the 20 year period at 52.48%

My actual increase in cost of living was 142.58%

The Fed,’s Treasury.GOV and BLS.GOV’s motivation

If inflation had been accurately reported since 1980 US debt service cost and the cost of all Federal programs who’s increases are tied to the BLS.GOV CPI such as Social Security would have left the US government insolvent over a decade ago.

The spread between the Federal debt in red and tax receipt growth in green would be have been far wider a lot sooner.

Orange = BLS.GOV reported CPI

Purple = Federal debt service cost

Green = US Federal tax receipts

Red = Federal debt

Blue = Social Security

Source Federal Reserve

Source Federal Reserve

As I see it US politicians long ago decided that they weren’t going to do something as unpopular as raising taxes, or as responsible as cutting budgets to balance a budget when the BLS.GOV can revise the CPI to generating trillions of dollars without having to get that pesky public or congressional approval.

This kind of attitude might have balanced a budget in the short term but it didn’t, not only did politicians the Fed, US Treasury and BLS.GOV essentially steal money from depositors, Social Security Recipients and the providers of all governmental goods and services who’s increases are tied to the CPI politicians unconscionably escalated governmental spending.

End result a debt to GDP ratio of 105% closing in on the World War II all time high of 113%

Source Federal Reserve

With revisions putting inflation near zero, deposit rates near zero and all increases tied to the “official CPI” near zero saving the US Treasury trillions of dollars budget deficits during economic stimulus still averaged 894 billion annually and remain above 400 billion.

Politicians, the Fed, US Treasury and BLS.GOV realize the revision well has finally run dry and there are only 4 options left

- Double taxes across the board

- Immediate and severe budget cuts across the board

- A combination much higher taxes and severe budget cuts

- Extremely aggressive dollar devaluation

Think of your self as a politician, we’re not talking about what’s best for the US in the long run, we’re talking about your best interest in the long run and the “speaking fees” you can crank out after you leave office, Regan 1 million, Trump 1 million, Bill Clinton 450K, Hilary Clinton 200K, Gore 150K, Palin 100K?

Potential outcomes

1) Double taxes, well that’s not going to work everyone that’s making money who can grab their laptop and plug into the internet in tax free country will leave. Who will be left to pay your 100K to 1 million nightly “speaking fees” after you leave office.

Case in point British Virgin Islands. $2,000 for government fees, a medical exam, a plane ticket and in 11 hours or less your on white sandy beach, if you don’t live the beach on you can drive to legally with a cocktail in your hand, once there order more as you bask in the sun. Example the British Virgin Islands

https://s0.wp.com/wp-content/themes/pub/twentyfifteen/js/html5.js

Facts about the British Virgin Islands

Taxation in the British Virgin Islands

Real Estate in the BVI for $2,000,000 USD or less

2) Immediate and severe budget cuts across the board, well considering only 45% of the US population has a job (143 million people).

Source Federal Reserve

The other 175 million might not like that too much, 8.75 million (5% of the work force) are unemployed and the other 166.25 million (52% of the population) don’t have jobs cutting benefits and programs isn’t going to generate votes.

Source Federal Reserve

3) A combination much higher taxes and severe budget cut, well we no that a very big no go it would just piss off everyone and you wouldn’t make it to the primaries.

4) Extremely aggressive dollar devaluation, YES we have a winner, no tax hikes, no budget cuts, The Fed and BLS.GOV can take care of the dirty work and you’ll have time to meet your favorite “speaker” at a suite at the Hay-Adams , pay her, her 1 hour “speaking fee” and be able to be back at the mansion in Cleveland Park to have dinner with the wife and kids.

What I don’t know

- Who will be running the United States in 2017 or the policies they’ll implement

- The impact these policies will have on the market

- When foreign investors will have had enough and liquidate US stocks, debt instruments and dollars that are all currently trading near their highs.

- The numbers the BLS.GOV will release to maintain the impression the US economy is in “recovery” and on track or how the the market will react.

What I do know

The overall US economic numbers are the worst in US history. They certainly do not support the representation that the “Great Recession” officially ended in 2009 and the US economy is in recovery. What they do show is “economic stimulus” for the US taxpayer, future generations of Americans and the US economy was the most costly policy failure in US history.

The US now is facing the worst debt crisis in its history without the tax receipts to service the Federal debt service cost if rates “normalized” much less pay this debt down.

Green = US Federal tax receipts

Red = Federal debt

Purple = Federal debt service cost

Source Federal Reserve

Source Federal Reserve

I know Non-US investors (like myself) now own US assets that are equivalent to 130% of the US GDP.

Non-US investors own over 40% of the total US Corporate Bonds and US Equities.

Non-US investors own over 55% of the marketable US Treasury debt

Source Council on Foreign Relations

I see the US equity markets now bouncing of record highs struggling to make higher highs.

Long term Treasury prices are near record highs with yields near record lows, instrument appreciation potential is nearly non existent.

Short term Treasuries same scenario

The dollar is coming off a 10 year high

Instrument price and currency risk for non US investors (like myself) is more in one day than any annual potential price appreciation, dividends or yields.

The only reason I’ve held off selling is to capture instrument price appreciation definitely not the dividend or interest income which are beyond pathetic.

Currently I can invest in 13 countries that have a higher credit ratings than the US, 18 that have the same or higher rating.

- The combined GDP for these countries exceeds the US’s

- Economic releases have proven to be more reliable

- Most have upside currency appreciation potential greater than the USD

- Many have the same or higher short term rates

- Most have far higher academic achievement for the youth that will be running their countries in the coming decades.

Unfortunate, harsh but true

As I see it BLS.GOV and the Fed’s creditability is no longer in the toilet, it’s already been flushed.

The Fed with the help of the BLS.GOV keeps telling us there is no inflation in order to justify the low rates, actual price increases tell me a completely different story.

Reality

Artificially low inflation justifies artificially low rates stripping savers and the free market economy of trillions of dollars to save the US Treasury the same trillions, not stimulate the economy.

Artificially low inflation

- Justifies stripping Social Security recipients of much needed cost of living increases removing trillions more from the economy to save the US Treasury the same trillions in cost of living increases, not to stimulate the economy.

- Saves the US Treasury trillions more in in every governmental expenditure increase that is tied to the BLS.GOV CPI, not stimulate the economy.

I think is should be pretty clear Economic stimulus was for the US Treasury and Banks not the US taxpayer, their children or their children’s children that will be picking up the tab.

The Fed keeps telling us we’ll see 8 to 15, 0.25% rate hikes by December 2018 if they’re right the US would become insolvent by debt service cost alone if debt service increased at the same pace.

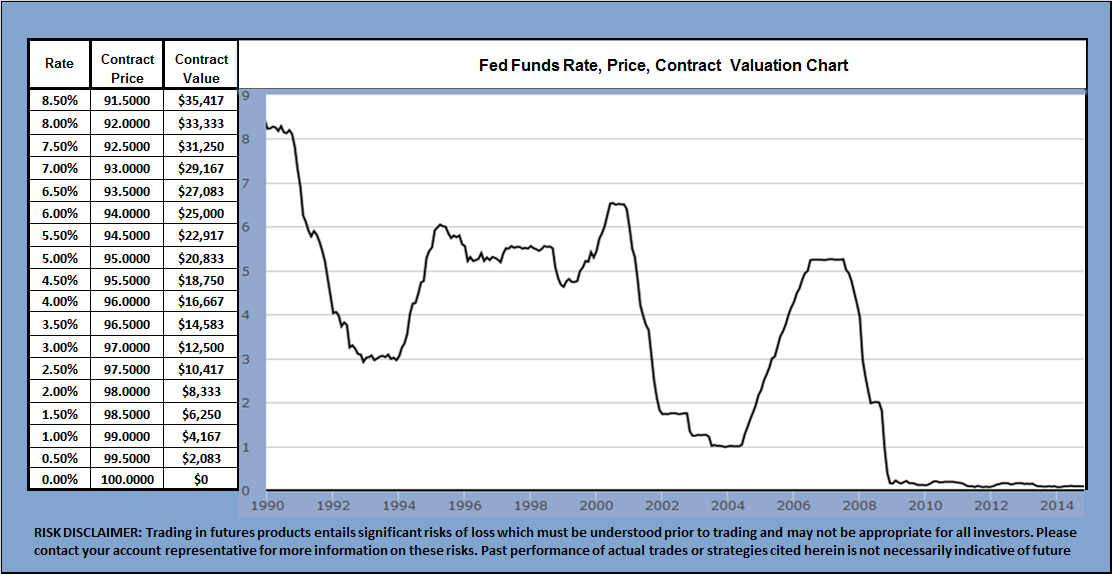

Where the world’s largest derivatives market is pricing rates and when

Market’s rate hike expectations from May 2011 through June 2016

A) May of 2011 3, 0.25% rate hikes by December 2018, the value of this spread was $1,875

B) January 2013 10, 0.25% rate hikes, value of this spread increased to $6,250.

C) Currently less than 2, 0.25% rate hikes are expected by the market by December 2018, spread value $1,250, a new low for the spread, rate hike expectations and Fed creditability.

D)If the Fed had creditability with the market the spread would be trading closer to 2.00 to 2.50 position value $6,250, not below 0.50 position value $1,250.

Click here to monitor the Dec 2016 Dec 2018 spread current 0.32

Metals are telling us the same

Platinum versus gold; In short platinum although 9 times more scarce than gold is an industrial metal, when the market is optimistic about industry and the economy platinum sells at a premium to gold, when the market believes the economy will continue to be in the sewer platinum sells at a discount to gold, the more pessimistic the market the deeper the discount platinum sells to gold, we’re near all time low with platinum selling at over a $3oo discount to gold.

Click here to monitor this spread currently at -$326.70

There are countless other spreads and indicators I track and they all are basically telling me the same thing, , that mother of all US asset and US dollar “corrections” is on the horizon.

Dollar devaluation is already in play

After the sub-prime meltdown the Fed, US Treasury and the BLS.GOV chose to devalue the dollar but not before they could finance the largest amount of debt in history for the longest period of time in history at the lowest rates in history.

How

When short term rates dropped to near zero any depositors desperate for any interest income at all were “sucked into” longer dated durations (5+ years)

As these investors shifted from shorter to longer dated durations for higher rates the Fed contained higher rates on these longer dated durations using strategies like the maturity extension program.

It’s taken the Fed, BLS.GOV and US Treasury over 7 years to accomplish debt with an average duration held greater than 5 years at and average interest paid less than 2.75% taxable.

Whatever happens to interest rates during the next 5 years as the dollar devalues US Debt service cost will remain relatively constant.

As the debt and equity markets struggle to make higher highs currency and instrument risk is more in one day than annual yields, dividends or asset appreciation potential.

Should the US debt and equity markets fail to make a significant higher high prior to China’s currency being recognized by the IMF as a world reserve or the US elections in November, Non US investors like myself will start aggressively liquidating US debt, equities and dollars and establish net new short positions in US markets.

Non US investors already have homes lined up for the proceeds of US asset and US dollar sales in any of the 13 countries that have a higher debt ratings than the US, most have the same or higher yields, most have better currency appreciation potential than the USD as it sells off from its 10 year high.

Domestic investors trying to preserve their wealth will join in on the selling as the market “corrects” many will establish net new outright shorts.

Selling will intensify, additional shorts will enter the market accelerating the move lower.

The Fed and US politicians will blame the selloff in stocks, debt instruments and the dollar on Non US investor selling, in part they will be correct.

They’ll focus the blame on China as Chinese investors sell US debt and US dollars for Renminbi after the Renminbi officially comes on line as a “free floating” world reserve currency this October. Chinese investors will take their money home to an appreciating currency, earning a higher interest rate in an economy that according to the World Bank will be larger then the US economy by 2019.

The US US Treasury, Fed and BLS.GOV will have China to blame for the mess they created

When the dollar devalues by more than 25% the Fed will have the excuse they need to fire up the quantitative easing printing press with tenacity creating trillions more dollars with keypunch entries backed by no tangible asset or income flow to intervene and cauterize the market’s hemorrhage.

The creation of trillions more dollars will eventually be inflationary once these trillions “trickle down” into the economy.

As the dollar devalues as a result of inflation the prices of Gold and all other tangible assets (including shares) will increase.

True inflation will rise above 10%, it could potentially rival the old high of 14.8%, I don’t know. What I do know and history has proven is when you increase the amount of money in circulation in any economy chasing after the same amount of goods and services prices rise.

The “official” BLS.GOV inflation will rise but remain dramatically below true inflation

Rates will rise but still be below BLS.GOV reported inflation and dramatically below true inflation. ( = negative rates of return and loss of true wealth for savers)

Incomes will rise but not nearly as quickly as true inflation( = declining lifestyle, sost of living versus constant standard of living)

Tax receipts will increase proportionally as the prices of goods and services rise. In theory you could have twice the amount of US dollars in circulation chasing after the same amount of goods and services doubling prices and increasing tax revenue by 100%.

As the majority of the current US debt is fixed at the lowest rates in history for the longest period of time in history US debt service cost will not rise as dramatically as true inflation and potentially remain below 1/2 a trillion per year.

End result

- Potentially twice the tax receipts generated by high inflation.

- A relatively constant debt service cost because s the majority of US debt is fixed

- The same savers who have been stripped of trillions of dollars by the largest negative rates of return in history for the longest period of time in history are about to have their buying power of their remaining savings in US debt and dollars cut in half all to save the Treasury.GOV the same trillions.

During the dollar’s devaluation the BLS.GOV will continue to misrepresent inflation is dramatically lower than actual inflation to contain debt service cost on new issues that need to be sold to finance future deficit spending, maturing issues that need to be refinanced and contain the cost on all other governmental expenses whose increases are linked to the official BLS.GOV CPI rate.

The damage will be severe to NON US investors no smart enough to get out as they own approximately 60% of all marketable US Treasury debt and have dollar devaluation exposure against their home currencies as the dollar tanks.

The US will survive but lose a great deal of creditability and face additional debt downgrades making it more difficult if not impossible to market new issues to foreign investors.

China’s GDP will surpass US GDP

The ratio between the growth in tax receipts relative to the national debt will improve dramatically from current levels while growth in debt service cost trickle slowly higher.

More money, relatively constant debt service cost

Green = US Federal tax receipts

Red = Federal debt

Purple = Federal debt service cost

Source Federal Reserve

I see no other out for the US Treasury

Enough of the bad news

The good news is bad news generates major market moves and powerful trends, it’s going to be a fun year for traders who are on their game and have strategies in place to capture the major market moves.

Time to brush on the sectors you have forgotten about, your shorting and collar strategies. Metals are sure to shine, debt instruments look like they be a downer (rates higher) and we should have the opportunity to pick up our favorite shares at much better prices after the selling hemorrhage stalls.

Few of my favorite stocks and ETFs to trade (both short and long)

- Apple (NASDAQ:(AAPL)

- NYSE, Bank of America Corporation(BAX)

- Microsoft (NASDAQ:MSFT)

- Alphabet ([[GOOG]], [[GOOGL]])

- Pfizer (NYSE:PFE)

- Cisco (NASDAQ:CSCO)

- Goldman Sachs (NYSE:GS)

- Moody’s (NYSE:MCO)

- Oracle (NYSE:ORCL)

- AT&T (NYSE:T)

- AbbVie (NYSE:ABBV)

- JPMorgan Chase (NYSE:JPM)

- Baxter International Inc (BAX)

- Bank of America Corporation (BAC)

- General Electric Company (GE)

- SPDR S&P 500 Trust ETF (SPY)

- ARCA, iShares MSCI Emerging Markets ETF (EEM)

- ARCA, SPDR S&P Metals and Mining ETF (XME)

- ARCA, Pfizer Inc. (PFE)

- Apple Inc. (AAPL)

- SPDR Gold Trust ETF (GLD)

- ARCA, iPath S&P 500 VIX Short-Term Futures ETN (VXX)

- ARCA, Market Vectors Gold Miners ETF (GDX)

- ARCA, Ford Motor Company (F)

- Financial Select Sector SPDR ETF (XLF)

- ARCA, iShares China Large-Cap ETF (FXI)

- ARCA, Shares Russell 2000 ETF (IWM) – NYSEARCA,

- SPDR Gold Trust GLD

- COMEX Gold Trust IAU

- Physical Swiss Gold Shares SGOL

- DB Gold Fund DGL

- DB Gold Double Long ETN DGP

- UltraShort Gold GLL

- Gold Trust OUNZ

- Ultra Gold UGL

- DB Gold Double Short ETN DZZ

- 3x Long Gold ETN UGLD

- DB Gold Short ETN DGZ

- 3x Inverse Gold ETN DGLD

- Gartman Gold/Yen ETF GYEN

- Gartman Gold/Euro ETF GEUR

- E-TRACS UBS Bloomberg CMCI Gold ETN UBG

- X-Links Gold Shares Covered Call ETN GLDI

Derivatives

- Precious metals

- Energy

- Debt instruments

- Currencies

- S&P 500

- Dow

- NASDAQ 100

- FTSE 100

- EuroStoxx 50

- Nikkei 225

The following exchanges can provide additional information

I’ll be writing follow ups providing specific strategies

Volatility will be high, trade with the trend, when possible use option collars to define your risk on trades and for the duration of the trading period.

Peter Knight

Click here for contact details

x

RISK DISCLOSURE STATEMENT

PROGRAM AVAILABILITY IS DEPENDENT ON YOUR COUNTRY OF RESIDENCY AND FINANCIAL STATUS

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. EXAMPLES OF HISTORIC PRICE MOVES OR EXTREME MARKET CONDITIONS ARE NOT MEANT TO IMPLY THAT SUCH MOVES OR CONDITIONS ARE COMMON OCCURRENCES OR ARE LIKELY TO OCCUR.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT.

IN ADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITHSTAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CAN ALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF ANY SPECIFIC TRADE PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR IN THE PREPARATION OF THE HYPOTHETICAL PERFORMANCE RESULTS AND ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL TRADING RESULTS.

BID/ASK SPREADS, BROKERAGE COMMISSION, CLEARING, EXCHANGE AND REGULATORY FEES WILL HAVE AN ADVERSE IMPACT ON THE NET OVERALL PERFORMANCE OF YOUR ACCOUNT. PRIOR TO MAKING A DECISION TO PARTICIPATE IN ANY INVESTMENT MAKE SURE YOU FULLY UNDERSTAND THE FEES ASSOCIATED WITH TRADING.

THE INFORMATION PROVIDED IN THIS REPORT CONTAINS RESEARCH, MARKET COMMENTARY AND TRADE RECOMMENDATIONS. YOU MAY BE SOLICITED FOR AN ACCOUNT BY ONE OF OUR REPRESENTATIVES OR EMPLOYEES. IT SHOULD BE KNOWN THAT THE REPRESENTATIVES OF OUR FIRM MAY TRADE FUTURES AND OPTIONS FOR THEIR OWN ACCOUNTS OR THOSE OF OTHERS. DUE TO VARIOUS FACTORS (SUCH AS MARGIN REQUIREMENTS, RISK FACTORS, TRADING OBJECTIVES, TRADING INSTRUCTIONS, TRADING STRATEGIES, AND OTHER FACTORS) SUCH TRADING MAY RESULT IN THE LIQUIDATION OR INITIATION OF FUTURES OR OPTIONS POSITIONS THAT DIFFER FROM THE OPINIONS AND RECOMMENDATIONS FOUND IN THIS REPORT.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE PERFORMANCE. THE RISK OF LOSS IN TRADING FUTURES CONTRACTS OR COMMODITY OPTIONS CAN BE SUBSTANTIAL, AND THEREFORE INVESTORS SHOULD UNDERSTAND THE RISKS INVOLVED IN TAKING LEVERAGED POSITIONS AND MUST ASSUME RESPONSIBILITY FOR THE RISKS ASSOCIATED WITH SUCH INVESTMENTS AND FOR THEIR RESULTS.

YOU SHOULD CAREFULLY CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR CIRCUMSTANCES AND FINANCIAL RESOURCES.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}