Defining risk using “option collars”

1) Procedure for a Collared Long Position

1.1) On the 15th of September 2017 was telling us the S&P is in a medium-term up trend and to structure trades for 11 to 29 days.

Enter a long futures position at 2,500.00

Contract value $125,000.00

1.2) Determine the profit objective

In this example I’m simplifying the profit objective procedure by extending the angle of the slope using the medium-term EMA9 chart by the maximum trade duration of 29 days to generate a profit objective of 2,550.00 contract value $127,500.00.

Profit Objective 2,550.00

Contract value $127,500.00

2) Collaring the trade

2.1) At the 2,550.00 profit objective I sell an out of the money, call option against the my long position at the closest strike price to the objective of 2,550,00.

2.2) I’ll chose an options expiration that is consistent with the maximum trade duration for the trade, in this example 29 days, 13th of October 2017.

2.3) When you sell a call against your 2,500.00 long futures position (covered call) you’re collecting option time premium, in this example we’ve collected 15.00 points or +$750.00.

How we objectively define risk

2.4) Using the collected premium from the covered call of 15.00 points, ($750.00) I buy a put option.

2.4) The put option purchased must have the same option expiration as the call we wrote, in this example the option expiration for the call we wrote is the 13th of October 2017, the put purchased must have the same expiration date.

2.5) The put strike price should be approximately the same distance from our 2,500.00 long entry as the call we wrote at the 2,550 objective (50 points).

2,500.00 entry – 50.00 = 2,4550.00, the put I purchase to define my risk should be at a strike of 2,450.00 or higher.

2.6) The option premium price paid for the put option to define risk should be approximately the same amount as what I’ve collected from the call I wrote. (In this example I’ve collected 15.00 points ($750.00) on the call, the put protection premium should cost me approximately 15.00 points ($750.00).

2.7) Purchase the 2,450.00 put with the same expiration date for 17.00 points ($850.00).

2.8) The put objectively defines my risk on the 2,500.00 long position for the duration of the trading period (entry date 15 September 2017 to 13 October 2017 expiration)

2.9) The put also negates any possibility of this position being stopped out for the duration of the trading period.

2.10) Summary

Long a futures contract at 2,500.00

Collected on the 2,550.00 call write, 15.00 points at the profit objective

Paid out on the 2,450.00 put purchase -17.00 points to objectively define risk

Net cost of the hedge = 2.00 points or $100.00, which defines risk on a contract worth $125,000 from the 14th of September 2015 until the 13th of October 2017.

3) Potential outcomes

3.1) The market stays the same and settles on the 13th of October 2017 at 2,500.00 unchanged from entry.

3.2) Trade Result

The call we wrote at 2,550 expires worthless, +15.00 points = +$750.00

The 2,500.00 long futures settles unchanged at 2,500.00 = $0.00

The 2,450 put purchased expires worthless, we lose 17.00 points = -$850.00

Total bid/ask spreads, commission, exchange & regulatory fees =-$159.78

All in net profit or loss = -$259.78

3.3) The market moves hard against us

The market drops from our entry price of 2,500.00 (contract value = $125,00.00) down 600.00 points -24.00% to 1,900.00 contract value $95,000 in “fast market action“.

If a percentage drop like this occurred, it would have no impact on the maximum risk of this collared position because we own the put.

The maximum risk (in this example) is the distance between our entry at 2,500.00 contract value $125,000.00 to where the put engages at 2,450.00, contract value $122,250.00, maximum loss $2,500.00 regardless if this market moves to zero.

3.4) Trade Result

Loss on the 2,500.00 long futures position (600.00) points = -$30,000.00

The call we wrote at 2,550.00 expires worthless +15.00 points =+$750.00

The put we own at 2,450.00 is profitable 533.00 points =+$26,650.00

Total bid/ask spreads, commission, exchange & regulatory fees =-$159.78

All in net loss = -$2,759.78

A $100.00 hedge prevented a potential loss on this position of $30,000.

3.5) The market moves higher in our favor

The established trend continues higher from our long entry of 2,500.00 contract value $125,000 to our profit objective of 2,550.00 contract value $127,500 on or before the 13th of October 2017.

3.6) Trade Result

Gain on the 2,500.00 long futures position 50.00 points = +$2,500.00

The covered call we wrote at 2,550.00 is offset by the futures, we also keep the 15.00 points in collected premium =+$750.00

The put we own at 2,450.00 expires worthless -17.00 points =-$850.00

Total bid/ask spreads, commission, exchange & regulatory fees =-$159.78

All in net profit or loss = $2,240.22.

4) Procedure for short positions

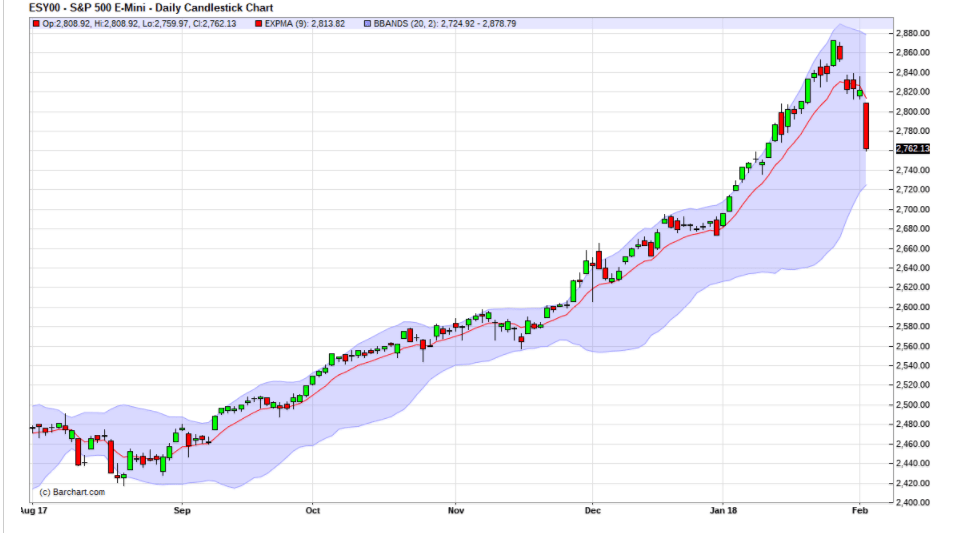

4.1) On the 1st of February 2018 (TIP) Trend identification procedure linked here is telling you the S&P is in a short-term downtrend and to structure a short trade for 2 to 10 days.

We enter a short futures position at 2,815.00

Contract value $140,750.00

4.2) Determine the profit objective

To simplify I am continuing the angle of the slope on the short-term EMA9 chart out 10 days to generate a profit objective of 2,740.00

Profit objective at 2,740.00

Contract value $137,500.00

5) Collar procedure

Short futures on 2 February 2018 at 2,815 (contract $140,750.00)

5.1) I write an out of the money, put option against my 2,815.00 short futures position at the strike price that is closest to the profit objective, in this example 2,740.00

5.2) I choose an options expiration that is consistent with the TIP defined trade duration (in this example the 9th of February 2018).

5.3) When I write an out of the money option against my short position I collect option premium, in this example I’ve collected 27.00 points or +$1,350.00.

Objectively Defining Risk

5.4) Using the collected premium of 27.00 points or +$1,350.00 from the sale of the 2,740.00 put I buy a call option.

5.5) The call option purchased must have the same option expiration as the put I wrote (in this example the 9th of February 2018).

5.6) The option premium price paid for the call option should be approximately the same amount or less than what I’ve collected from the put write (in this example I collected 27.00 points or +$1,350.00).

5.7) The call strike price should be approximately the same amount from entry. In this example I’m short futures at 2,815.00 , I written an out of the money put at my profit objective 75.00 points below my 2,815 short entry , the call I purchase should be at a strike of 2,815.00 + 75.00 = 2,890.00 or lower.

5.8) I purchase the 2,890.00 call with an expiration date of the 9th of February 2018 for 16.00 points or –$800.00.

5.9) The call objectively defines risk on my 2,815.00 short position for the duration of the trading period (entry date 2nd of February 2018 to the 9th of February 2018 expiration)

5.10) The call negates any possibility of this position being stopped out for the duration of the trading period.

5.11) Summary

Short a futures contact at 2,815.00

On the put write at my profit objective of 2,740.00 I’ve collected 27.00

I’ve paid out 16.00 points on the 2,890.00 call to objectively define my risk

Net cost of the hedge = +9.00 points or $550.00, in this example we I’m getting paid to define risk on a contract worth $140,750 from the 2nd of February 2018 to the 9th of February 2018 .

6) Potential outcomes for this trade

6.1) The market stays the same and settles on the 9th of February 2018 unchanged from our entry at 2,815.00.

6.2) Trade Result

The put wrote at 2,740.00 expires worthless, I keep the 27.00 points = $1,350.00

The 2,815.00 short futures settles unchanged at 2,815.00 = $0.00

The 2,890.00 call purchased expires worthless, I lose 16.00 points = -$800.00

Total bid/ask spreads, commission, exchange & regulatory fees = -$159.78

All in net profit or loss = +$390.22

6.3) The market moves hard against us

The market rallies from my short entry at 2,815.00 (contract value = $144,500.00) 300.00 points +10.66% to 3,115.00 contract value $155,750 in “fast market“ action.

If a rally like this occurred it would have no impact on the maximum risk of this collared position because I own the call.

The call objectively defines my risk on the this short position for the duration of the trading period. The maximum risk (in this example) is the distance between my entry at 2,815.00 contract value $140,750.00 to where the call engages at 2,890.00 contract value $144,500.00

6.4) Trade Result

Loss on the 2,815.00 short futures position 300.00 points = -$15,000.00

The put I wrote at 2,7400 expires worthless +27.00 points =+$1,350.00

The call I own at 2,890.00 is profitable by 209.00 points =+$10,450.00

Total bid/ask spreads, commission, exchange & regulatory fees = -$159.78

Net loss = -$3,359.78.78

In this example I was paid $+550.00 to prevent a potential loss of $15,000

6.5) Market moves lower in my favor

The trend continues lower from my short entry at 2,815.00 on the 1st of February 2018 contract value $140,750.00 to my profit objective of 2,740.00 contract value $137,000 on or before the 9th of February 2017.

6.6) Trade Result

Gain on the 2,815.00 short futures position 75.00 points = $3,750.00

The put I wrote at 2,740.00 is offset by the short futures position, I keep the +27.00 points in collected option time premium = +$1,350.00

The call I purchased at 2,890.00 expires worthless -18.00 points = -$800.00

Total bid/ask spreads, commission, exchange & regulatory fees = -$159.78

All in net gain or loss = $4,140.22

7) S&P Collar Spreadsheet

- Open with Excel

- Click OK

- Enable editing

- Enable content

If you have questions or need help with this procedure please schedule an online review or send me a message

Regards,

Peter Knight Advisor

Contact

____________________________________________________________________________

Privacy Notice

Disclosure

Peter Knight

Peter Knight